How to build a clean Cost Breakdown Structure (CBS) and avoid fragmented cost categories across cost centers

If you manage project budgets, cost control, forecasting, or earned value, one mistake can quietly damage your entire reporting structure before the project even gains momentum:

creating different cost categories for each cost center, instead of using one standardized cost category structure across the project.

It may look harmless at the beginning. Teams often create categories locally, based on habit, department preference, station, package, or work location. But over time, this turns into a fragmented coding system that makes budgeting, reporting, KPI tracking, and financial control unnecessarily difficult.

For organizations that want lean, transparent, and scalable project financial management, this is exactly the kind of mistake that must be avoided.

At RABIO (Rapid Business Information Organizer), an open-source budgeting software designed to organize projects and control financial activities such as budgets, costs, KPIs, earned value, forecast, and projections, the Cost Breakdown Structure (CBS) is not just an accounting convenience. It is a core governance principle.

In this article, we explain why fragmented cost categories are a problem, what a proper CBS should look like, and how standardized cost coding improves project control.

What Is the Cost Coding Mistake?

A common setup error in project controls is this:

- Cost Center A has its own cost categories

- Cost Center B has different cost categories

- Cost Center C introduces another logic

- Similar work is described differently depending on the area, team, or package

Instead of having a single project-wide cost category structure, each cost center starts behaving like its own mini-project.

The result is confusion.

For example, the same type of resource or activity may appear under one code in one cost center and under a completely different code in another. The description may be almost identical, but because the coding logic changes by location or department, the data can no longer be compared cleanly.

This is not simply a naming issue. It is a structural control failure.

Why This Happens

This mistake usually appears when there is no clear governance model for project coding. Teams may:

- build cost codes independently

- mix cost center logic with category logic

- confuse CBS with local operational descriptions

- create new categories every time a new area or station is added

- copy old practices from previous projects without standardization

In many cases, the root cause is simple:

there is no single coding philosophy guiding the Cost Breakdown Structure.

Without a consistent framework, every team codes “what makes sense” locally. Unfortunately, what makes sense locally often becomes a problem globally.

Why Different Cost Categories per Cost Center Is a Serious Problem

1. It destroys comparability

If the same work is coded differently across cost centers, you cannot compare costs consistently.

You lose the ability to answer basic questions such as:

- How much are we spending on engineering across the whole project?

- What is the total cost of installation activities?

- Which resource type is over budget?

- Where are labor costs increasing faster than planned?

If categories are inconsistent, the answers become unreliable.

2. It weakens budget control

Budget control depends on structure. If every cost center uses its own categories, then budget baselines become fragmented.

Instead of one coherent financial model, you end up with parallel coding systems that do not roll up properly. This makes control slower, more manual, and more error-prone.

3. It makes earned value and KPIs less trustworthy

Metrics like earned value, cost performance, forecast variance, and projections only work well when the underlying coding is consistent.

If data is coded differently across cost centers, KPI calculations may still produce numbers, but those numbers will not always be meaningful.

A dashboard is only as reliable as the structure behind it.

4. It complicates reporting

Finance teams, project controllers, and managers need reports that are easy to read and explain.

When cost categories differ by cost center, reporting requires mapping tables, manual adjustments, and repeated explanations. Instead of simplifying decision-making, the system creates administrative work.

5. It makes scaling difficult

As the project grows, coding chaos grows with it.

A structure that works for a few cost centers may become unmanageable when the project expands. What starts as a small inconsistency can become a major reporting and governance problem later.

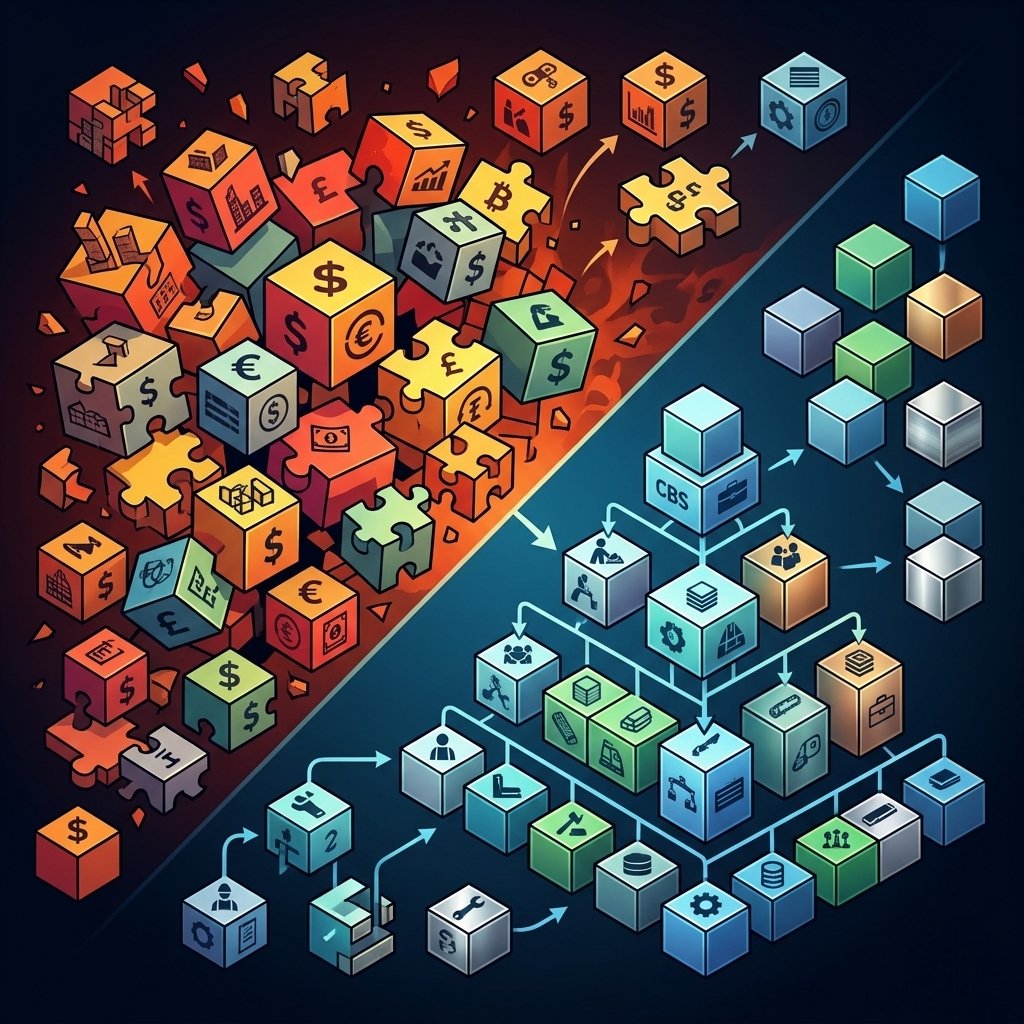

The Correct Approach: One Cost Category Structure Across the Project

A robust Cost Breakdown Structure (CBS) should use:

- one common cost category model

- consistent category definitions

- clear separation between cost center and cost category

- standardized coding rules across the full project

This means:

- the cost center identifies where the cost belongs

- the cost category identifies what type of cost it is

These are not the same thing and should not be merged.

For example:

- Cost Center = Civil Works / Area A / Station 1

- Cost Category = Labor

- Cost Category = Materials

- Cost Category = Equipment

- Cost Category = Subcontracting

The same category structure should repeat across all cost centers.

That is what makes aggregation, comparison, forecasting, and project-wide visibility possible.

Cost Center vs Cost Category: The Distinction That Must Stay Clear

This distinction is fundamental.

Cost Center

A cost center represents a responsibility area, location, function, package, department, or segment of the project where costs are collected.

Cost Category

A cost category represents the nature of the cost itself, such as:

- labor

- materials

- equipment

- subcontractors

- engineering

- logistics

- overhead

A cost center answers:

Where is the cost assigned?

A cost category answers:

What kind of cost is it?

When teams create unique cost categories inside each cost center, they blur this distinction. Once that happens, the CBS loses consistency and the financial model becomes harder to control.

What a Good CBS Looks Like

A well-designed CBS is:

Standardized

The same logic is applied everywhere.

Scalable

New cost centers can be added without inventing new category structures.

Comparable

The same activity or resource can be analyzed across all project areas.

Reportable

Costs roll up cleanly for dashboards, reports, and executive summaries.

Forecast-ready

Forecasting and projections can be built on stable data.

Earned value-friendly

KPIs are more meaningful when cost data is structurally consistent.

Example of the Wrong Setup

Imagine a project with multiple stations or work fronts.

In one station, a resource is coded under:

- Mechanical Installation / Internal Team / Field Execution

In another station, the same type of work is coded under:

- Site Mechanical Support / Operations Labor / Execution Team

In a third station, it appears under yet another variation.

These may look similar operationally, but financially they are not aligned. Reporting them together becomes difficult, and comparing actual vs budget across stations becomes weak or misleading.

The organization ends up spending time translating data instead of controlling it.

Example of the Right Setup

A better model would be:

Cost Centers

- Station 1

- Station 2

- Station 3

Common Cost Categories

- Labor

- Materials

- Equipment

- Subcontracting

- Engineering

- Indirect Costs

Now each station uses the same category logic. This allows project controls teams to:

- compare labor costs across stations

- consolidate material costs at project level

- forecast equipment demand more accurately

- measure earned value with more confidence

- identify cost overruns earlier

This is how a CBS should support decision-making.

Why This Matters for Budgeting Software

Budgeting software should not just store numbers. It should enforce clarity.

A good project controls platform must help organizations structure data in a way that supports:

- budget creation

- cost collection

- variance analysis

- forecasting

- projections

- KPI measurement

- earned value management

This is where Rapid Business Information Organizer (RABIO) brings value.

As an innovative open-source budgeting software, RABIO is designed to help teams organize projects and control financial activities in a simple and lightweight software platform. By using a structured Cost Breakdown Structure, RABIO supports better consistency in the way budgets and costs are organized across the project lifecycle.

When the CBS is designed correctly from the beginning, the software becomes a real decision-support tool instead of a passive data repository.

Best Practices to Avoid CBS Fragmentation

To avoid creating different cost categories per cost center, follow these best practices:

1. Define the cost category dictionary early

Before execution begins, create a single project-wide list of approved cost categories with clear definitions.

2. Separate structure from description

Operational descriptions may vary by location, but cost categories should remain standardized.

3. Do not let each team invent local coding

Coding freedom may feel flexible, but it creates reporting inconsistency.

4. Use cost centers for ownership, not for category design

A cost center should collect costs, not redefine the financial taxonomy.

5. Validate the CBS before loading budgets

A poor structure entered early will affect every report later.

6. Keep the model simple

A lean coding structure is easier to maintain, explain, and scale.

7. Align budgeting, reporting, and KPI logic

If the same structure supports budget, actuals, forecast, and earned value, project control becomes much stronger.

The Strategic Benefit of a Simple Structure

Many project teams think complexity gives control. In reality, clarity gives control.

A simple and well-governed CBS offers:

- cleaner data

- better roll-up reporting

- faster budget reviews

- easier variance analysis

- more reliable forecasts

- clearer earned value metrics

- less administrative correction work

Standardization does not reduce flexibility. It creates the foundation for useful flexibility.

Final Thoughts

The mistake is clear:

do not create different cost categories for every cost center.

A cost center is not a separate financial universe. It is just one part of the project structure. If each cost center uses its own category logic, the project loses comparability, consistency, and control.

The right approach is to define one common cost category structure and apply it consistently across all cost centers through a proper Cost Breakdown Structure (CBS).

For organizations using modern project controls and budgeting tools such as RABIO, this is not a minor modeling detail. It is a critical condition for accurate budgeting, cost management, earned value tracking, forecasting, and performance visibility.

If you want your project financial data to stay simple, light, and useful, start with the structure.

Because once coding chaos enters the system, every report becomes harder than it should be.